Accounting and tax support is provided by certified public accountants and tax accountants. The role of certified public accountants is to perform audits under the Certified Public Accountant Law, while tax accountants engage in typical tax agent services such as the preparation of tax documentation and giving tax consultations under the Certified Tax Accountant Law. Additionally, both professions provide additional services such as business consulting.

Source: JETRO, Taxes in Japan: Consultation with Specialists on Accounting and Tax Support

The Japan’s Generally Accepted Accounting Principles (J-GAAP) are issued by the Financial Service Agency (FSA) and Accounting Standards Board of Japan (ASBJ). It is one of the four sets of accounting standards listed companies in Japan can currently choose from to use to file their consolidated financial statements. The other three accounting standards are Designated IFRS, US-GAAP and Japan’s Modified International Standards (JMIS). In 2019, over 30% of the companies listed on the Tokyo Stock Exchange had adopted or plan to adopt IFRS standards, the ratio has increased rapidly in recent years.

All basic accounting principles for any domestic company are based upon the following 7 pillars namely,

- true and fair reporting,

- an orderly system of bookkeeping,

- a distinction between capital surplus and earned surplus,

- a clear disclosure,

- consistency,

- prudence and

- in accordance with reliable accounting records and facts.

The typical but non-mandatory fiscal year in Japan runs from 1 April until 31 March of the next year, different from our Western style where often the fiscal years run similar to the calendar year.

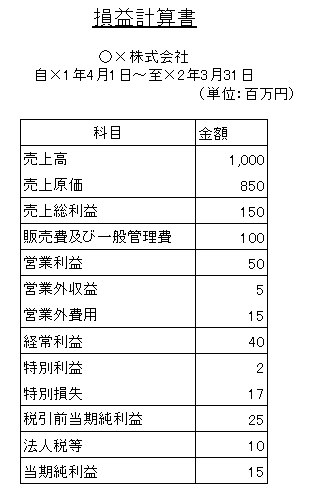

Financial documents of a fiscal year closing usually consists of the following documents being, the Balance Sheet (B/S) (taishakutaishohyou), the Profit and Loss statement (P/L) (sonekikeisansho), the statement of changes in net corporate assets (kabunushi shihon douhen doukei sansho) and where needed, also explanatory notes for the aforesaid financial statements.

{kind=link}

Any joint-stock company (Kabushiki Kaisha, often abbreviated as KK) with its registered corporate address in Japan, shall give public notice of its balance sheet (for a large company, its balance sheet [B/S] and profit and loss [P/L] statement) without delay after the conclusion of the annual shareholders meeting. Publicly listed companies are also required to publish their quarterly and annual securities reports.

Not only accounting principles but also taxation systems will differ profoundly, depending upon the status of the business entity which can vary from representative or branch office over the typical 100% subsidiary as permanent establishment called Kabushiki Kaisha to the lesser known Limited Liability Company (LLC) and Limited Liability Partnership (LLP).

Source: Rob Van Nylen, Accounting and Taxes (EU-Japan Centre for Industrial Cooperation Report)