The Centre quarterly newsletter, June 2026 issue, is now available.

In this issue:

Last chance…

Japan’s tax reform measures for FY2019: Will CT finally go up?

2019 is already destined to be an historic year: - The first year in the new Reiwa era. However there is another major event planned for this fiscal year as well: Will Japan finally have its increase in consumption tax (CT) to 10%, after having been postponed repeatedly?

2019 is already destined to be an historic year: - The first year in the new Reiwa era. However there is another major event planned for this fiscal year as well: Will Japan finally have its increase in consumption tax (CT) to 10%, after having been postponed repeatedly?

This time again, there are voices for another postponement, as global economic headwinds are gaining force. On the other hand, demands such as transforming the country’s social security system into something that works for all generations and ensuring that the country’s fiscal health is turned towards a path of improvement, make a raise in CT inevitable.

Many of the tax measures taken for FY 2019 are to be seen in the light of the impeding increase in CT, and designed to soften the effects of the increased tax burden on Japanese consumers and prevent them from pulling their purse’ strings too tight.

Beside measures for Japanese consumers, a variety of tax measures to support SMEs in their business activities and in particular to promote smooth business succession are also implemented this year. JTPP Helpdesk summarizes the main changes for FY 2019 below.

Corporate taxation

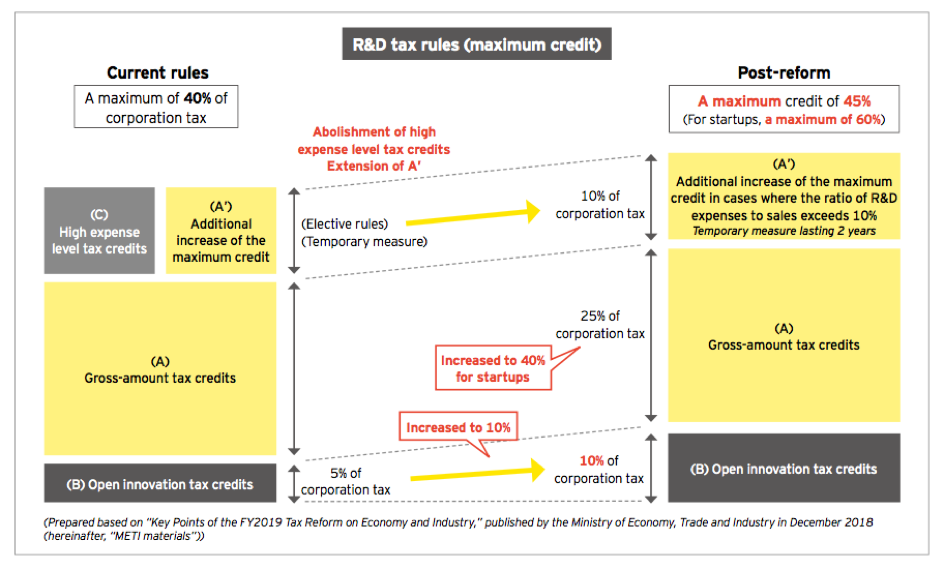

Revision of R&D Tax rules to promote innovation

To promote active investment in R&D, special corporate tax credits available for conducting experimental research etc. will be revised.

- Max. gross amount tax credits available for start-ups involved in R&D increased from 25% to 40% of corporation tax of that fiscal year;

- Additional increase of the maximum credit (10% of applicable FY) in cases where the ratio of R&D expenses to sales exceeds 10%;

- Credit rate curve for R&D expenses will be revised.

- Application period of the special measure designating a maximum credit rate of 14% will be extended by 2 years.

- Open innovation tax credits will be increased to 10% of corporation tax.

EY has summarized the various measures in a useful graph, were one can see that start-ups will be able to claim a maximum credit of 60% under the new rules.

Fiscal incentives for R&D by SMEs

Presently, special measures are in place that provide a preferential tax credit limitation (Upper limit of 35%) where the ratio of increased R&D exceeds 5%. This threshold is increased to 8% and the applicable period will be extended for another 2 years.

Support for capital investments by small and intermediate businesses:

- Continuation of the investment promotion tax system for SMEs and the exemption measure for a lower corporate tax rate for SMEs

- Continuation of SME management reinforcement tax measure:

- Immediate depreciation or a 10% tax credit

- To attain 1% increase in productivity

- Package investment of 5% ROI

- Continuation of the SME investment promotion tax measure:

- 30% special depreciation or 7% Tax credit

- Continuation of Retail and service revitalization tax measure:

- 30% special depreciation or 7% tax credit

- Immediate depreciation or a 10% tax credit

- Continuation of SME management reinforcement tax measure:

- In the regional future investment promotion fiscal system, the special depreciation deduction rate is increased from 40% to 50% and the tax credit rate is increased from the current 4% to 5%.

- Establishment of special depreciation measure to promote investment in disaster prevention measures for SMEs.

- Special depreciation of 20% for disaster prevention and remediation related assets such as earth-quake resistance systems and equipment (generators, drainage pumps, flooding prevention boards and shutters etc.).

- In order to qualify the businesses must have their prevention plan approved by METI

- Creation of a regional tax system for the sustainable development of cities and regions

- Others:

- Increase of the exemption rate for disaster insurance premiums from 5% to 6%

- Reform and improvement of the special depreciation system for medical equipment to promote more efficient use of expensive medical equipment , support the regional medical systems and lower workhours of medical personnel

- Continuation of the exemption for corporate taxation for SMEs

- For SMEs with annual income of less than 8 million JPY the rate will remain lower at 15% instead of the regular 19%

- For those with an annual income larger than 8 million JPY the rate of 23.2% applies

Individual income taxes

- Expansion of home-loan deductions for housing loans taken out in a period of 12 months after the increase of CT from October 1, 2019

- Deductions for a period of 13 years instead of current 10 years

- New establishment of forest environment tax and forest environment donation tax

- Reform of the Hometown tax system

- Individual inhabitant taxes tax relief measure to counter child poverty

Property taxes

- Establishment of a tax measure for business succession for sole proprietors

- For a limited period of 10 years, succession tax and gift tax payment for the succession of capital assets for various kinds of businesses can be 100% deferred. For example:

- Land, buildings

- Machinery and equipment

- Cars and trucks

- Cattle, fruit/vineyards

- Intangible assets

- For a limited period of 10 years, succession tax and gift tax payment for the succession of capital assets for various kinds of businesses can be 100% deferred. For example:

- Reform of the lump-sum asset transfer tax relief measures for educational funds, marriage or child support

Consumption taxes

- Reform of automobile body taxation

- Decrease of the automobile taxes after October 1st, 2019

- Reform of the classification into environmental impact categories of automobiles

- Improvement of the tax-free system for foreign travellers, allowing more vendors in the regions to offer tax free products.

International taxes

- Deal with the impact of the Base Erosion and Profit Shifting (BEPS) project

Tax payment infrastructure

- In reply to the diversification of economic transactions, facilitate the necessary tax payment infrastructure (E-Tax, enabling keeping of electronic records etc.)

More information about the FY 2019 Tax reforms is available here:

- Ministry of Finance (In Japanese)

- EY Tax alerts Japan

- The Small and Medium Enterprise Agency (In Japanese)

- KPMG Tax Newsletter

- PWC Tax Update Newsletters

Published: April 2019

EU-Japan Centre for Industrial Cooperation

Joint venture established in 1987 by the European Commission (DG GROW) and the Japanese Government (METI) for promoting all forms of industrial, trade and investment cooperation between the EU and Japan.

Copyright © 2026 EU-Japan Centre